20th April, 2026

Australian advisors and their clients are increasingly asking a pointed question: in a market with no shortage of talented managers, why is consistent outperformance so elusive? The answer lies not in the quality of ideas, but in the structural constraints placed on how those ideas can be expressed.

Traditional long-only funds can only profit when a stock goes up. They are structurally limited in their ability to act on negative views—a manager who believes a stock is overvalued can, at best, hold less of it than the benchmark. This is a significant constraint, and it is one that long/short equity strategies are specifically designed to overcome.

Long/short equity is a broad category of strategies that hold both long positions (stocks the manager expects to outperform) and short positions (stocks the manager expects to underperform). The short positions are typically funded by borrowing shares, selling them, and seeking to repurchase them later at a lower price. The resulting proceeds can then be reinvested into additional long positions.

This family of strategies spans a wide spectrum, and understanding where a fund sits on that spectrum matters for advisors.

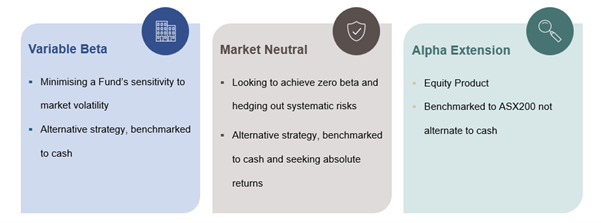

At one end sits the market-neutral fund—constructed to have near-zero net exposure to the market. These funds aim to profit purely from the spread between their long and short books, regardless of market direction. They tend to have low beta, low correlation to equity indices, and are usually housed within alternatives allocations.

At the other end are concentrated long/short funds, which maintain meaningful net long exposure but use shorts to express high-conviction negative views. These can carry significant market sensitivity and behave more like active equity funds with extra tools.

In the middle—and of particular relevance to Australian investors—sits the active extension strategy. Sometimes called a 130/30 (or 135/35, 140/40), these funds maintain a 100% net long exposure to the market, typically benchmarked to an index like the ASX 200. They are permitted to short a defined percentage of the portfolio (say, 30%), with the proceeds reinvested into additional longs (hence “extension”). The result: the same market beta as a traditional equity fund, but a materially expanded opportunity set.

The ASX 200 is a concentrated index, with the top 10 stocks representing a substantial share of total market capitalisation. In long-only portfolios, underweighting these large-cap names is difficult—there is a limit to how negative you can be on a stock that makes up 8% of the benchmark. Active extension strategies remove this constraint, allowing managers to express their full conviction without the distortions imposed by benchmark composition.

Additionally, Australian markets have historically shown good dispersion at the stock level—meaning individual companies diverge meaningfully in their performance. High dispersion is the environment in which skilled active managers can thrive, and in which short books can add the most value.

Long/short equity isn’t always about taking more risk—it’s about removing the structural handcuffs that prevent skilled managers from fully expressing their views. Active extension strategies generally offer the same market exposure as traditional equity funds while significantly expanding the opportunity set for alpha generation. For Australian portfolios navigating a concentrated index, this can be a meaningful advantage.

The structure makes sense on paper—but the proof is in the outcomes. In our next insight, Capturing Alpha, we take a clear-eyed look at the evidence and show how active extension strategies have the potential to strengthen risk-adjusted returns without changing the fundamentals of your equity allocation.

Disclaimer:

This material is prepared by Paradice Investment Management Pty Ltd (ABN 64 090 148 619 AFSL No 224158) (Paradice, we or us) to provide you with general information only. This material is not intended to constitute advertising or advice (including investment advice or security, market or sector recommendations) of any kind. These materials are not to be distributed and must not be copied, reproduced, published, disclosed or passed to any other person at any time without the prior written consent of Paradice.

It may contain certain statements, opinions and projections that are based on the assumptions and judgments of Paradice with respect to, among other things, economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Paradice. Because of the significant uncertainties inherent in these assumptions, opinions and judgments, you should not place undue reliance on these statements and before any action or decision is taken on the basis of this material you should obtain appropriate independent professional advice, as necessary.

The information and opinions contained herein are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents.

Subscribe to our newsletter for updates.

Visit our site for individuals and financial advisors.

Visit our site for institutional investors.