March, 2026

Paradice Australian Equities Team

Paradice Australian Equities Fund March 2026 Commentary

Performance

The Fund returned -347bps after ongoing management costs, underperforming the S&P/ASX 200 Total Return Index (ASX200) by -186bps over the quarter to 31 March1.

Key Contributors/Detractors

Positives

Negatives

Key Changes

Purchases

Sales

Market Review

The MSCI World Total Return Index dropped 3.2% (USD) and the S&P/ASX 200 Total Return Index eased 1.6%2 in the March quarter as the USA went to war with Iran. Brent oil prices spiked 94.5% (USD) as the Strait of Hormuz closed, which skewed inflation risks to the upside and drove US 2-year Treasury yields 32 bps higher. The NASDAQ Total Return Index (USD) fell 7.0% as concerns of Artificial Intelligence (AI) disruption were an additional headwind to valuation compression from higher rates. Concerns around Private Credit also surfaced as retail investors requested redemptions more than ‘gate’ limits at some funds, perhaps due to worries over lending to businesses being disrupted by AI.

Macro data deteriorated in March around the world in response to the Middle Eastern conflict but remains solid. The JP Morgan Global Composite PMI in March dropped 2.3 points sequentially, which is the largest one-month drop since the invasion of Ukraine3. Both the Global Manufacturing and Services PMI indices dropped, and declines occurred across all major global regions. However, as reported in recent JP Morgan research the PMI reading of 51.0 does remain expansionary and is consistent with ‘trend-like’ 2.5% global GDP growth. Inflation prints in the quarter were in our opinion, largely too backward-looking to be relevant, given the jump in oil prices we expect yet to flow into inflation. The US Fed held rates flat and said, “inflation progress is disappointing, risks are rising, and cuts may not come”. US futures removed more than two 25bp cuts they had priced to occur over the calendar year and now imply an approximately flat outcome. In Australia, the RBA rose rates 25bp to 4.1% as monthly CPI inflation at 3.7% in February remained high versus their 2-3% target. Futures here now imply over two 25bp rate hikes over the year, which is an increase from ~1x previously.

The Australian February reporting season was solid with an ~1% EPS beat on average but again is relatively backward looking. During the quarter Energy stocks leapt 37.7% on the 94.5% (USD) surge in Brent Oil and 109.6% (USD) spike in JKM Asian LNG. Materials rose 3.9% on a 49.5% (USD) rise in Spodumene, 18.2% (USD) advance in Aluminium and 8.1% (USD) rise in Gold, while Iron Ore was flat. Banks increased 2.2% on faster credit growth and persistent low loan losses. AI disruption risks weighed heavily on IT stocks which fell 28%4. Consumer Discretionary stocks eased 14.6% on more cautious outlooks due to a weakening consumer. AREITS underperformed on the higher rate outlook.

ESG Engagement5

During the quarter we undertook a total of 44 engagements in which we discussed ESG matters with 31 companies relevant to the strategy. The majority of meetings during the quarter were held at the board or executive level, with most with the CEO following the release of financial results. In addition to climate change, ethical conduct and environmental management were notable topics of interest for the team.

In the quarter, we had two executive-level meetings, and one ESG-focused meeting with BHP Group (BHP). We continued our engagement on Traditional Owner relationships and permitting in the Iron Ore business, seeking updates on agreement modernisation efforts. We also met the new CEO, whose appointment was announced in the period, and were pleased to hear him state that safety was his top priority and a prerequisite to BHP maintaining operational excellence. Timelines for its heavy fleet decarbonisation appear to be slipping, however, which may cast doubt on the achievability of its interim emissions target so we will closely monitor the next climate update at the full year results.

Additionally, we had two meetings with Insurance Australia Group (IAG). In our post results meeting we got an update on management of perils exposure, while we also met with members of IAG’s natural perils team for a deep dive on the insurer’s understanding and management of physical climate risk. The team supported our understanding of how the increase in secondary perils due to climate change is changing the reinsurance market. IAG also demonstrated how it could reduce risk through product design and direct interventions, which is complemented by its policy advocacy work. In particular, advocating for government investment in adaptation and climate-informed town planning which is significantly more cost effective than disaster response. We also tested IAG’s response to managing social licence as affordability becomes an issue in climate-exposed areas.

Outlook

At the time of writing, the US and Iran have just announced a two-week ceasefire, although details remain unclear on many issues, including the reopening of the Strait of Hormuz, and so concerns are likely to remain over whether the ceasefire will stick. At this point we are concluding that we are likely past ‘peak fear’, on the basis that neither side can continue to take further war pain, but the risk of further spikes in warring activity remains.

The outlook for equity markets over the next quarter therefore could be volatile but directionally neutral. The Fund’s beta is slightly under 1.0x consistent with a cautious risk stance. We see moderate economic growth, fiscal stimulus in the US and Australia, stable interest rate cuts in the US and increases in Australia, and slightly more attractive valuations in some sectors. Higher inflation and even possibly stagflation are the main risks to equity markets in addition to an elongated war.

The JP Morgan Global Composite PMI reading of 51.0 is consistent with ‘trend-like’ 2.5% GDP growth. U.S. real GDP growth is expected to be ~2%6 in 2026 boosted by greater fiscal stimulus from Trump’s One Big Beautiful Bill Act (OBBB). At the end of March, the US futures market was pricing an approximately flat rate outlook for the rest of the year and the US S&P500 market was trading on 19.6x December 2026 Price/Earnings ratio.

Australian GDP is also expected to grow at ~2%6, aided by fiscal stimulus. The RBA’s more ‘hawkish’ rate policy reflected in Australian futures market pricing of over two 25bp rate increases this year will be a headwind for the consumer and rate sensitive sectors. The duration of elevated fuel prices and inflation data will be important drivers of further changes to rate policy. Divergent rate outcomes between Australia and the USA should result in upward pressure on the AUD and support higher commodity prices. As at the time of writing, the S&P/ASX200 trades on 16.6x June 2026 Price/Earnings ratio.

Portfolio Positioning

The Fund is modestly overweight Materials. The Fund is overweight ‘bulk’ commodities including aluminium, via BHP and Fortescue, as Chinese demand is stimulated, via Alcoa. PLS is held as demand for lithium stabilises. Lynas is held for strategic rare earth opportunities. It is now underweight gold equities, via Newmont and Northern Star, following the commodity price becoming extended.

Financials are underweight, via Banks, but we have reduced the size of the underweight. Banks are trading on record valuations. However, despite fundamentals appearing to peak for some time now, we have been surprised at ongoing strength. The Bank underweight has been reduced following a better-than-expected CBA NIM and credit growth outcome, and ANZ quarterly trading update from a cost management perspective. The Fund is overweight insurers QBE and IAG as they benefit from an insurance hardening pricing cycle.

The Fund holds Macquarie on solid earnings growth via their commodities trading business and asset realisations.

The Fund is positioned in selective Industrial stocks with what we have determined as, growing earnings and attractive valuation. These include Brambles as it continues to grow earnings and generate free cashflow, SGH (formerly Seven Group) where earnings are seemingly supported by a sustained equipment replacement cycle, and Qantas who enjoys robust domestic demand and pricing power. The Fund holds overweight positions in Xero and Seek, following underperformance and becoming oversold on AI concerns that we conclude are now overdone.

Within the Consumer sectors, the Fund is overweight A2 Milk and Treasury Wine. From our assessment, A2 is capitalising on market disruptions to grow market share and Treasury Wine has strong valuation support. The Fund also holds neutral positions in supermarkets.

The Fund is neutral Healthcare, via ResMed, as it continues to deliver strong earnings growth in a benign competitive environment.

The Fund holds some small caps where we see appreciable upside for idiosyncratic reasons.

The Fund is underweight Real Estate Investment Trusts where earnings growth remains soft.

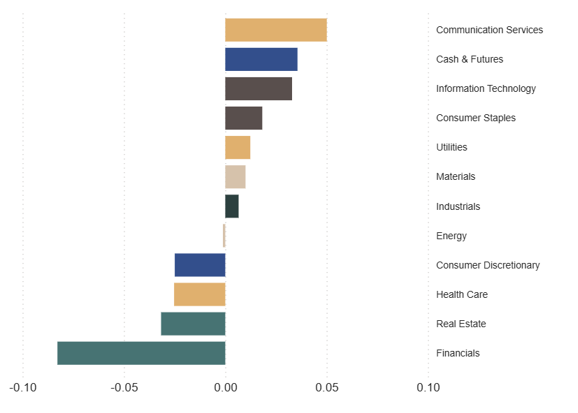

The Fund’s active positioning by sector7 as of 31 March 2026 is as follows

Top 5 active positions (Overweight)

For further details on fund positioning please refer to the Paradice Australian Equities Quarterly Fact Sheet.

For any other questions in relation to the Fund, please contact distribution@paradice.com.

1All indices are Total Return Indices unless otherwise stated.

2For the purposes of comparison commentary is quoted in Australian dollar terms and Australian sector returns refers to the S&P/ASX 200 Total Return Index unless stated otherwise..

3JP Morgan Global Economic Research, 7 April 2026.

4Technology Sector..

5This fund is not an ESG product please see the PDS for further information on our ESG considerations

6Source: Bloomberg consensus

7Paradice portfolio sector assignment is based on GICS. Source: Factset and Paradice. Relative allocation is based on the market value of each position expressed as a % of the total portfolio relative to benchmark weights.

Disclaimer:

This material is prepared by Paradice Investment Management Pty Ltd (ABN 64 090 148 619 AFSL No 224158) (Paradice, we or us) to provide you with general information only. It is not intended to take the place of professional advice and you should not take action on specific issues in reliance on this information.

This material is not intended to constitute advertising or advice (including investment advice or security, market or sector recommendations) of any kind. In addition, this material represents only the views of the Paradice Australian Equities team as at the time of release and is not intended, and may not, represent the views of Paradice or any of the other investment teams at Paradice.

Equity Trustees Limited (ABN 46 004 031 298, AFSL No. 240975) (Equity Trustees) is the responsible entity of, and issuer of units in, the Paradice Australian Equities Fund (Fund). Equity Trustees is a subsidiary of EQT Holdings Limited (ABN 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX:EQT).

It may contain certain forward looking statements, opinions and projections that are based on the assumptions and judgments of Paradice with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Paradice. Because of the significant uncertainties inherent in these assumptions, opinions and judgments, you should not place undue reliance on these forward looking statements. For the avoidance of doubt, any such forward looking statements, opinions, assumptions and/or judgments made by Paradice may not prove to be accurate or correct. You should perform your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. Specific securities identified herein are not representative of all securities purchased, sold, or recommended by the Fund previously or in the future. Following publication of this material, the investment teams at Paradice may transact or continue to transact in any of the securities covered herein, and may be positive, negative or neutral at any time hereafter regardless of our initial conclusions, or opinions.

The content of this publication is current as at the date of its publication and is subject to change at any time. It does not reflect any events or changes in circumstances occurring after the date of publication.

You should consider your own needs and objectives and consult with a licensed financial adviser when deciding whether the Fund is suitable for you. Past performance should not be taken as an indicator of future performance. You should also read the current Product Disclosure Statement before making a decision about whether to invest in this product and the Target Market Determination available at www.paradice.com . A Target Market Determination is a document which describes who this financial product is likely to be appropriate for (i.e. the target market), and any conditions around how the product can be distributed to investors. This material is not to be copied, reproduced or published at any time without the prior written consent of Paradice. Neither Paradice, Equity Trustees, nor any of their respective related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained in this publication or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this material.

The information and opinions contained herein, including information obtained from third party sources which are considered to be reliable, are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents.

Copyright© 2026 Paradice

Contributors:

Julia Weng

Subscribe to our newsletter for updates.

Visit our site for individuals and financial advisors.

Visit our site for institutional investors.