December, 2025

Paradice Australian Equities Team

Paradice Australian Equities Fund December 2025 Commentary

The portfolio returned -213bps, underperforming the S&P/ASX 200 Total Return Index (ASX200) by 112bps over the quarter net of fees.1

Key Contributors/Detractors

Positives

Negatives

The Fund undertook a -50% revaluation of a ~100bps active holding in CTD on 3 December 2025 following the company’s update to the market on 28 November 2025 that a portion of its European revenues from FY23-25 may need to be restated and possibly refunded which could lead to cash impacts. The revaluation was undertaken with consideration to precedents for accounting discrepancies, peer performance since the suspension from quotation, potential reputational impact resulting in loss of customers, and possibility of a capital raise. Further revaluation may be appropriate as more information becomes available.

Key Portfolio Changes

Purchases

Sales

Market Review

The ASX200 ended 2025 with a muted -1% return for the December quarter. For the year 2025, the ASX200 delivered a solid +6.8%2 (+10.3% including dividends). Key global indices fared relatively better, with the S&P 500 up +17.9%, FTSE100 up 35.1% and Nikkei225 up 29.3% (all Total Return Indices and in USD) for the calendar year 2025.

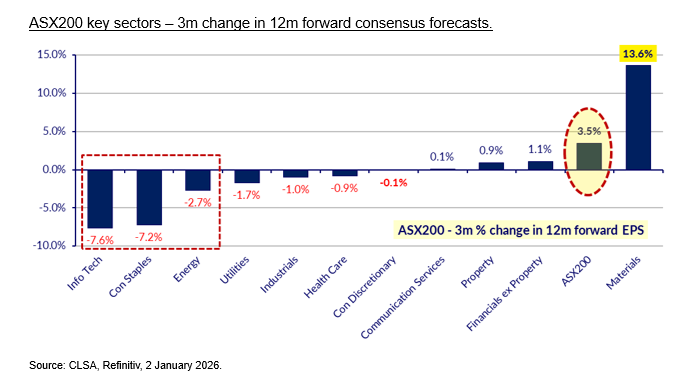

During the December 2025 quarter, markets rotated out of earlier winners (Technology and growth sectors) into cyclical commodity stocks. Materials were by far the best performing sector +13.0% on the ASX200, driven by record prices for precious metals and critical minerals including gold, copper, lithium, rare earths and resilience in iron ore prices. Sustained strength in commodity prices have triggered significant earnings upgrades. On the other hand, Information Technology (-26.0%), Consumer Discretionary (-11.7%), and Healthcare (-9.9%) saw a sharp reversal as investors questioned the relatively high valuation multiples paid, and there were some meaningful earnings disappointments.

Australian and US economic data appear to support different interest rate trajectories. In the US, the Federal Reserve continued cutting rates, as headline inflation slowed to 2.7% in December 2025, close to the Fed’s target. In contrast, CPI in Australia ended the year around 3.8% (as of October 2025), with ongoing inflation persistence a concern for the current rate cutting cycle. This could drive upward pressure on the AUD, which has historically been supportive for commodity prices.

Outlook

Moderate GDP of c2% is expected for Australia and the US in 2026. The dominant macro driver for equities markets remains the direction, pace and credibility of interest rate cuts. The bond market is currently pricing in circa 2 rate cuts in US, ending 2026 at a cash rate of 3.1%.

Meanwhile, the bond market is pricing in circa 2 rate increases in Australia, ending 2026 at a cash rate of 4.0%. Given the diverging interest rate expectations and current differentials, this could put upward pressure on the AUD (and in turn support higher commodity prices).

The second theme is whether investors’ perception of AI will change and move from “hype” to “proof”. AI has been a dominant driver of returns in the US supporting Technology, Utility and certain Materials stocks over the past few years. However, given the increased circularity of AI deals and the increased capex intensity of AI infrastructure build outs, and a rise in debt-fuelled investment, there have been notable increase in apprehension towards the sector in late 2025 e.g. Oracle is down c40% from its highs in 2025.

China is expected to maintain a GDP target of “around 5%” for 2026. Thus far in January, it has reportedly earmarked 62.5b RMB (Cus$9B) for expanded consumer trade-in subsidies, and approved a 295b RMB (Cus$42b) stimulus package for infrastructure modernisation.

Top 5 active positions (Overweight)

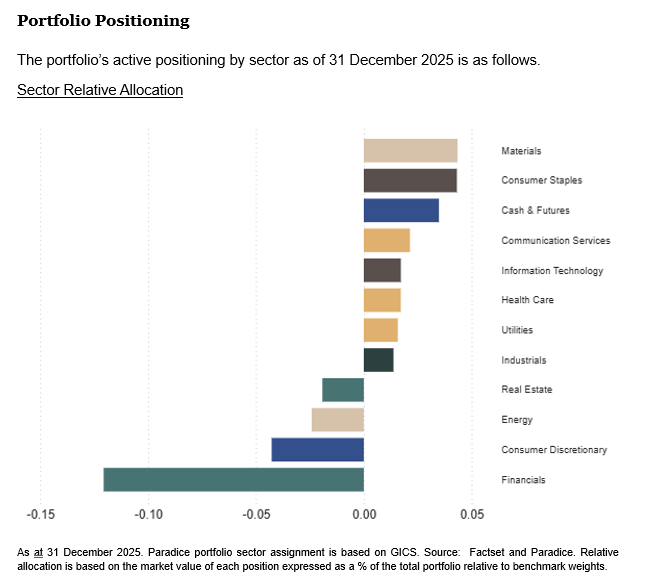

The portfolio is modestly defensively positioned as the multiple de-rate across growth sectors continues to weigh on the market. There is stark divergence of earnings revisions across the sectors, with Materials the only sector to have seen earnings upgrades in response to higher commodity prices. We believe Materials will continue to outperform in the short term driven by earnings upgrades and attractive starting multiples. Our preferences remain select gold, aluminium, rare earths, lithium and iron ore exposures.

Elsewhere, the portfolio is selectively positioned in stocks where we believe the market is overlooking potential earnings upgrades and where valuation is palatable. We are Overweight Consumer staples and Communications, principally through exposures in Coles, Treasury Wine Estates (TWE), A2 Milk and Seek. We have added to TWE post management’s update in December where EPS revisions were rebased by -30%, which we deem to be sufficiently conservative.

The portfolio has added a number of small caps where we believe there is appreciable upside for idiosyncratic reasons. A few examples are below:

The portfolio is underweight Financials principally due to Banks where valuations are at very stretched levels despite a lacklustre earnings growth profile.

For any other questions in relation to the portfolio, please contact distribution@paradice.com.

For further details on fund positioning please refer to the Paradice Australian Equities Quarterly Fact Sheet.

1Past performance of the Fund is not a reliable indicator of future performance. The value of an investment in the Fund may rise or fall. Returns are not guaranteed by any person. Fund returns are calculated before tax, after ongoing management costs and any accrued performance fees, and assumes the reinvestment of distributions.

2S&P / ASX 200 Price Return Index

Disclaimer:

This material is prepared by Paradice Investment Management Pty Ltd (ABN 64 090 148 619 AFSL No 224158) (Paradice, we or us) to provide you with general information only. It is not intended to take the place of professional advice and you should not take action on specific issues in reliance on this information.

This material is not intended to constitute advertising or advice (including investment advice or security, market or sector recommendations) of any kind. In addition, this material represents only the views of the Paradice Australian Equities team as at the time of release and is not intended, and may not, represent the views of Paradice or any of the other investment teams at Paradice.

Equity Trustees Limited (ABN 46 004 031 298, AFSL No. 240975) (Equity Trustees) is the responsible entity of, and issuer of units in, the Paradice Australian Equities Fund (Fund). Equity Trustees is a subsidiary of EQT Holdings Limited (ABN 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX:EQT).

It may contain certain forward looking statements, opinions and projections that are based on the assumptions and judgments of Paradice with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Paradice. Because of the significant uncertainties inherent in these assumptions, opinions and judgments, you should not place undue reliance on these forward looking statements. For the avoidance of doubt, any such forward looking statements, opinions, assumptions and/or judgments made by Paradice may not prove to be accurate or correct. You should perform your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. Specific securities identified herein are not representative of all securities purchased, sold, or recommended by the Fund previously or in the future. Following publication of this material, the investment teams at Paradice may transact or continue to transact in any of the securities covered herein, and may be positive, negative or neutral at any time hereafter regardless of our initial conclusions, or opinions.

The content of this publication is current as at the date of its publication and is subject to change at any time. It does not reflect any events or changes in circumstances occurring after the date of publication.

You should consider your own needs and objectives and consult with a licensed financial adviser when deciding whether the Fund is suitable for you. Past performance should not be taken as an indicator of future performance. You should also read the current Product Disclosure Statement before making a decision about whether to invest in this product and the Target Market Determination available at www.paradice.com . A Target Market Determination is a document which describes who this financial product is likely to be appropriate for (i.e. the target market), and any conditions around how the product can be distributed to investors. This material is not to be copied, reproduced or published at any time without the prior written consent of Paradice. Neither Paradice, Equity Trustees, nor any of their respective related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained in this publication or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this material.

The information and opinions contained herein, including information obtained from third party sources which are considered to be reliable, are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents.

Copyright© 2025 Paradice

Contributors:

Julia Weng

Subscribe to our newsletter for updates.

Visit our site for individuals and financial advisors.

Visit our site for institutional investors.