26th May, 2026

This year marks an extraordinary milestone – the 20th anniversary of the Principles for Responsible Investment (PRI). Not only is this a significant milestone for the responsible investment movement more broadly, but it’s also a good moment for us to reflect on what that commitment looks like in practice.

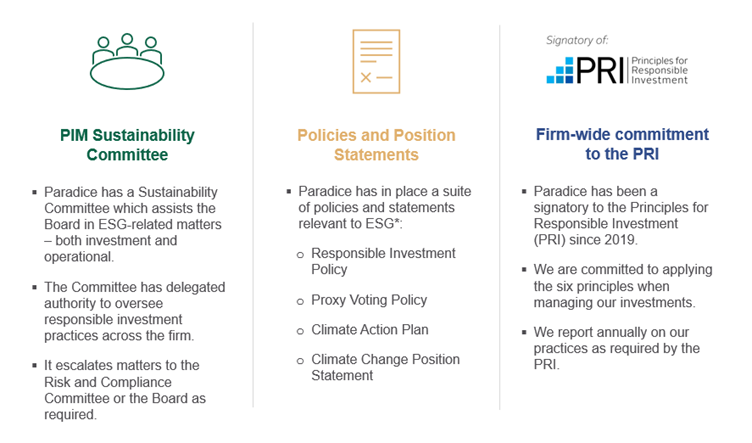

Paradice has been a PRI signatory since 2019, and our commitment has been grounded in a clear conviction that integrating ESG factors into investment analysis is consistent with fiduciary duty. ESG factors can have a real bearing on the long-term financial performance of the companies we invest in and taking them seriously helps us make better informed investment decisions on behalf of our clients.

To mark the occasion, we want to do more than acknowledge the anniversary. Below, we outline the governance structure and policies that underpin how we approach responsible investment at Paradice. We also highlight two multi-year engagements which demonstrate how we put those principles into practice, using our position as an investor to drive meaningful outcomes for our clients and the companies we own on their behalf.

Our approach to responsible investment is built on three pillars: an active Sustainability Committee that oversees our ESG commitments, clear policies and position statements that guide our decision-making, and our firm-wide commitment to the PRI — together forming the governance foundation from which our ESG integration and stewardship activity flows.

Governance frameworks and policies only mean something if they translate into action. The engagements below span several years and represent some of the more substantive examples of our stewardship in action. An active approach to company engagement is an ongoing and integral part of how we manage our portfolios, and these case studies bring that engagement to life.

The situation: Rio Tinto’s 2020 destruction of Juukan Gorge, and cultural heritage of the PKKP traditional owners, significantly undermined the company’s social licence to operate. It also underscored the importance for companies in the resources sector to have strong relations with their local traditional owners and to appropriately protect cultural heritage. For Rio Tinto in particular, given the failing at Juukan Gorge, it significantly increased its exposure to potential ongoing reputational risks and loss of social licence were it not to significantly improve its approach to cultural heritage. With iron ore operations across the Pilbara impacting the lands of multiple traditional owner groups, including some with Native Title determinations, we thought this necessitated deep and ongoing engagement.

What Paradice did: Immediately after Juukan Gorge, through engagement alongside other shareholders, we sought, what we determined as, appropriate accountability in the first instance, and then a necessary uplift in the company’s approach to managing traditional owner relations and protecting cultural heritage. Overtime our engagement focus shifted to looking for evidence that new ways of working were embedded within operations and that the company had the necessary internal capabilities and expertise. In the last two years, we have been particularly focused on the intersection of cultural heritage and water as we have observed water becoming a priority area for several traditional owner groups. Bodies of water can be sacred sites but are also important to maintaining traditional knowledge and culture. The combination of resource companies’ use of water for their activities with climate change-driven droughts has seen water in the Pilbara become more scarce and contested. We see water efficiency measures and greater use of desalinated water as part of the solution to protect water-related cultural heritage. We have engaged on water and cultural heritage with Rio Tinto multiple times since 2024, including with the Board and Executive Team. We have advocated for the acceleration of the modernisation of its agreements with traditional owners and greater consideration being given to benefits beyond royalty payments. On water, we have encouraged the expansion in capacity of a key project.

What the outcome was: In the months following Juukan Gorge, a commitment to an internal review and leadership change was secured, which saw the resignation of three executives and eventually the Chair. Rio Tinto made changes to its organisational structure to elevate the social performance function and added a director of indigenous heritage to its Board. Over the subsequent four years, Rio Tinto progressively expanded its cultural heritage uplift to its global operations as well. More recently, the company has progressed desalination in the Pilbara. The Dampier Seawater Desalination Plant was initially announced in June 2023 with a planned 4GL capacity. In March 2026, we were pleased to see Rio Tinto announce a joint venture with the WA Government to complete the $1.1 billion plant and expand its capacity to 8GL. Its announcement noted this would “considerably reduce groundwater take and help protect sites of environmental and cultural importance”.1 We continue to engage Rio Tinto on its agreement modernisation process but welcome this significant investment in water.

The situation: As an oil and gas company producing fossil fuels, Santos sits at the intersection of the energy transition. While its products may still be needed to meet energy demand for decades while systems transform to low carbon sources of generation, Santos must still act to reduce its climate transition-related risks. Of its overall emissions profile, its Scope 3 emissions dominate (those associated with the consumption of its product), but the production of oil and gas still directly generates significant operational emissions (Scope 1 and 2). As these emissions are more within Santos’ control, in our engagement with the company over the past five years we have encouraged it to produce its oil and gas as responsibly as possible.

What Paradice did: In years of engagement with Santos at both the Board and Executive level, we have regularly encouraged the company to invest in emissions reduction initiatives on average meeting four times a year. This has included where this has not been a regulatory requirement and the cost has been material. In our view this is an appropriate mitigation of its transition risk and supports its efforts to maintain social licence. In particular, we have encouraged a beyond-compliance approach to measurement and maintenance in order to reduce fugitive methane emissions (leaks and losses during processing), and that the company pursue carbon capture and storage (CCS) technologies.

What the outcome: We have been pleased to see Santos develop CCS capabilities, in particular through the Moomba CCS facility. Commissioned in 2024, the facility this month recorded 2 million tonnes of carbon stored in its first 18 months of operation, estimated to be the emissions equivalent of taking 826,000 cars off South Australian roads.2 Santos is looking to build a commercial carbon storage business for third-party emissions and has reported capacity to expand CCS at Moomba. Separately, it is advancing a CCS project at Bayu-Undan.

Responsible investment isn’t a destination — it’s an ongoing discipline. The PRI’s 20th anniversary is a reminder of how far the industry has come, but for us the more important measure is what we do year on year as active, engaged owners. These examples are a snapshot of that work. As the expectations on investors continue to evolve, our commitment to meaningful engagement will only deepen.

* The Australian business (Pty) and US business (LLC) have in place different policies and statements, reflecting their different operational jurisdictions.

Disclaimer:

This material is prepared by Paradice Investment Management Pty Ltd (ABN 64 090 148 619 AFSL No 224158) (Paradice, we or us) to provide you with general information only. This material is not intended to constitute advertising or advice (including investment advice or security, market or sector recommendations) of any kind. This material may not represent the views of all investment teams at Paradice. It may contain certain forward looking statements, opinions and projections that are based on the assumptions and judgments of Paradice with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Paradice. Because of the significant uncertainties inherent in these assumptions, opinions and judgments, you should not place undue reliance on these forward looking statements. For the avoidance of doubt, any such forward looking statements, opinions, assumptions and/or judgments made by Paradice may not prove to be accurate or correct. The content of this publication is current as at the date of its publication and is subject to change at any time. It does not reflect any events or changes in circumstances occurring after the date of publication. The information and opinions contained herein, including information obtained from third party sources which are considered to be reliable, are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents.

Subscribe to our newsletter for updates.

Visit our site for individuals and financial advisors.

Visit our site for institutional investors.