April, 2026

Paradice Australian Equities Team

Paradice Australian Equities Fund April 2026 Commentary

Performance

The portfolio returned 229bps, and outperformed the S&P/ASX200 Total Return Index (ASX 200) by 11bps over the month net of fees1.

Key Contributors/Detractors

Positives

Negatives

Market Review

The MSCI World Total Return Index rebounded 10.2% (USD) in April with markets reacting to the Middle Eastern ceasefire and strong US earnings that also drove the US S&P 500 up 10.5% (USD). The unemployment rate fell 0.1 percentage points to 4.3%, and the US economy added 178,000 jobs in the most recent nonfarm payrolls report, based on March data, well above the Dow Jones estimate of 59,000. The Federal Reserve held rates steady at 3.50–3.75% at its April FOMC meeting.

The ASX 200 Total Return Index rose only 2.2% lacking the strong earnings benefit and small technology weighting. Materials rose 4.3% on slightly better commodities pricing, with Spodumene lifting 16.7% (USD) on supply cuts and restocking, while Aluminium, Gold and Iron Ore were all flat. Information Technology bounced 13.25% on improving offshore sector sentiment.

Healthcare was the worst performing ASX 200 sector, falling 8.7%, with Cochlear warning on weak demand and margins. Within Consumer Staples, which dropped 4.1%, Woolworths warned on rising fuel costs and supplier cost pressure, and several smaller stocks also flagged weaker consumer sentiment. Energy eased 2.7% as Brent oil backed off 3.7% (USD) and JKM LNG fell 16.0% (USD) amid news of the ceasefire.

Outlook

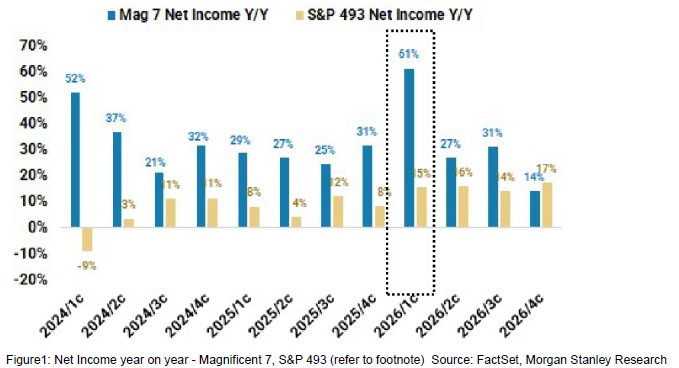

The US earnings season is nearing completion, and the strength and breadth of EPS revisions is in our view surprisingly firmly to the upside. 2026 consensus earnings have been revised higher to with the ‘Magnificent 7’ expected to grow for the S&P4932, with the divergence mostly attributed to AI spend.

Whilst hyperscaler and semiconductor earnings have been major contributors to this resiliency, the breadth of upward revisions has also been driven by Financials, Industrials and Consumer cyclicals. Specifically, 1Q EPS surprise for the median S&P 500 stock is 6%, the strongest it has been in 4 years, and S&P 500 median stock earnings growth is 16%.

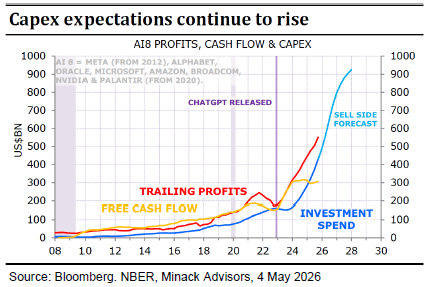

Big tech continues to lift AI investment plans. As referenced in recent research, prior to the reporting season the sell-side expected As of early May they expect $735 billion and $905 billion, respectively. Spending by unlisted companies such as OpenAI and Anthropic are additional, with flow on impacts on “picks and shovels” of the AI supply chain.

On the other hand, we are cautious on the outlook for the Australian economy given the combined impact of tightening policy conditions and sharper price and volume impact from the ongoing global fuel supply shock. We are assessing the speed and depth of a domestic slowdown, which is thus far materialising in modest home price declines in Sydney and Melbourne and softer home sales data in April as per updates from Mirvac and Stockland.

Select consumer facing companies such as JB Hifi, Supercheap and Flight Centre have also flagged softer sales as a result of a lower consumer sentiment. With the trimmed mean inflation (stripping out volatile items like fuel) in Australia stubbornly high at 3.3% in March 2026, the RBA likely has little choice but to stay hawkish to tame inflation expectations. The FY27 Federal Budget could further act as a hand brake on the economy with some slowing in spending growth (from elevated levels) and potential for tax increases (capital gains, negative gearing).

Portfolio Positioning

The outlook for equity markets could be volatile but directionally we are slightly optimistic. Although the ceasefire is fragile, we conclude that we are past ‘peak war fear’, on the basis that we expect neither side is willing to continue to take further war pain. There has seemingly been signs of intent from both sides to de-escalate and reopen the Strait of Hormuz.

We have modestly reduced the defensiveness of the portfolio in anticipation that the fuel-induced inflation and growth impact emanating from the Middle East conflict would be temporary. We have also rotated exposure away from domestic cyclicals towards select offshore earners where growth is likely to rebound sooner. During April, Telstra, Newmont and IAG have been modestly reduced. Positions in Macquarie, NAB and Aristocrat were added.

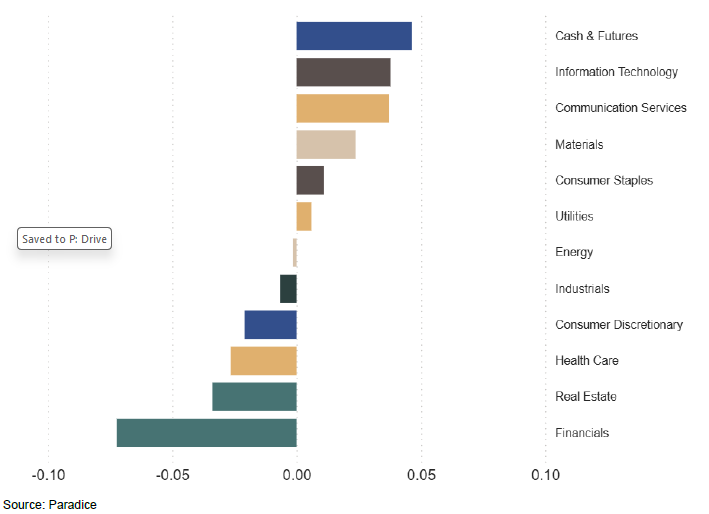

The Fund’s active positioning by sector as of 30 April is as follows.

For further details on fund positioning please refer to the Paradice Australian Equities Quarterly Fact Sheet.

For any other questions in relation to the Fund, please contact distribution@paradice.com.

All MSCI data is the property of MSCI. No use or distribution without written consent. Data provided “as is” without any warranties. MSCI and its affiliates assume no liability for or in connection with the data. Please see complete disclaimer in https://paradice.com/au/terms-conditions/)

1All indices are Total Return Indices unless otherwise stated.

2S&P 493 represents the S&P 500 constituents excluding the Magnificent 7.

Disclaimer: This material is prepared by Paradice Investment Management Pty Ltd (ABN 64 090 148 619 AFSL No 224158) (Paradice, we or us) to provide you with general information only. It is not intended to take the place of professional advice and you should not take action on specific issues in reliance on this information.

This material is not intended to constitute advertising or advice (including investment advice or security, market or sector recommendations) of any kind. In addition, this material represents only the views of the Paradice Australian Equities team as at the time of release and is not intended, and may not, represent the views of Paradice or any of the other investment teams at Paradice.

Equity Trustees Limited (ABN 46 004 031 298, AFSL No. 240975) (Equity Trustees) is the responsible entity of, and issuer of units in, the Paradice Australian Equities Fund (Fund). Equity Trustees is a subsidiary of EQT Holdings Limited (ABN 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX:EQT).

It may contain certain forward looking statements, opinions and projections that are based on the assumptions and judgments of Paradice with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Paradice. Because of the significant uncertainties inherent in these assumptions, opinions and judgments, you should not place undue reliance on these forward looking statements. For the avoidance of doubt, any such forward looking statements, opinions, assumptions and/or judgments made by Paradice may not prove to be accurate or correct. You should perform your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. Specific securities identified herein are not representative of all securities purchased, sold, or recommended by the Fund previously or in the future. Following publication of this material, the investment teams at Paradice may transact or continue to transact in any of the securities covered herein, and may be positive, negative or neutral at any time hereafter regardless of our initial conclusions, or opinions.

The content of this publication is current as at the date of its publication and is subject to change at any time. It does not reflect any events or changes in circumstances occurring after the date of publication.

You should consider your own needs and objectives and consult with a licensed financial adviser when deciding whether the Fund is suitable for you. Past performance should not be taken as an indicator of future performance. You should also read the current Product Disclosure Statement before making a decision about whether to invest in this product and the Target Market Determination available at www.paradice.com . A Target Market Determination is a document which describes who this financial product is likely to be appropriate for (i.e. the target market), and any conditions around how the product can be distributed to investors. This material is not to be copied, reproduced or published at any time without the prior written consent of Paradice. Neither Paradice, Equity Trustees, nor any of their respective related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained in this publication or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this material.

The information and opinions contained herein, including information obtained from third party sources which are considered to be reliable, are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents.

Copyright© 2026 Paradice

Contributors:

Julia Weng

Subscribe to our newsletter for updates.

Visit our site for individuals and financial advisors.

Visit our site for institutional investors.