10th April, 2026

The conversation around AI and software disruption has become increasingly noisy and SaaS company valuations have come under pressure as the market questions how sustainable some business models will be as AI models and agents become more capable.

Whilst we cannot have certainty, we believe the market may be overestimating the intermediary risk AI poses to many SaaS companies on the ASX200. In our view AI is a useful tool which enables SaaS to do more with less, rather than replace them entirely and likely places greater emphasis on enduring drivers of business success such as data ownership, regulatory depth and customer trust.

The old model was simple. Users worked through a SaaS interface—dashboards, workflows, integrations—which sat on top of systems of record holding the underlying data.

AI is compressing this. Autonomous agents increasingly do the work directly, squeezing the traditional UI layer as value shifts in two directions—up to the AI layer, and down to the systems of record that agents rely on. We think of this as the “thin middle” squeeze.

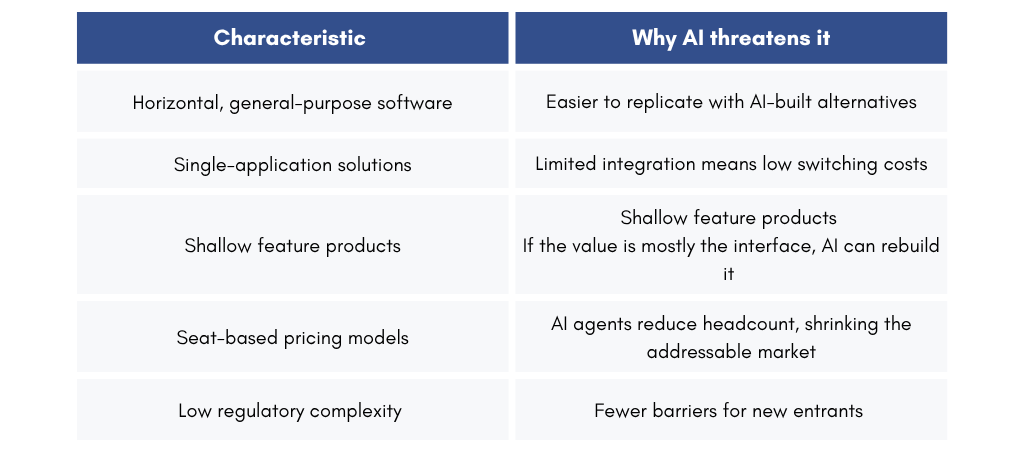

SaaS businesses whose main value is their interface—rather than their data or workflow integration—face the most pressure.

AI makes it significantly easier to build features. What once took months of engineering can now be prototyped in days. This represents a genuine leap forward in innovation and the speed of product launches. However, AI doesn’t lower barriers to:

Where we see higher disruption risk:

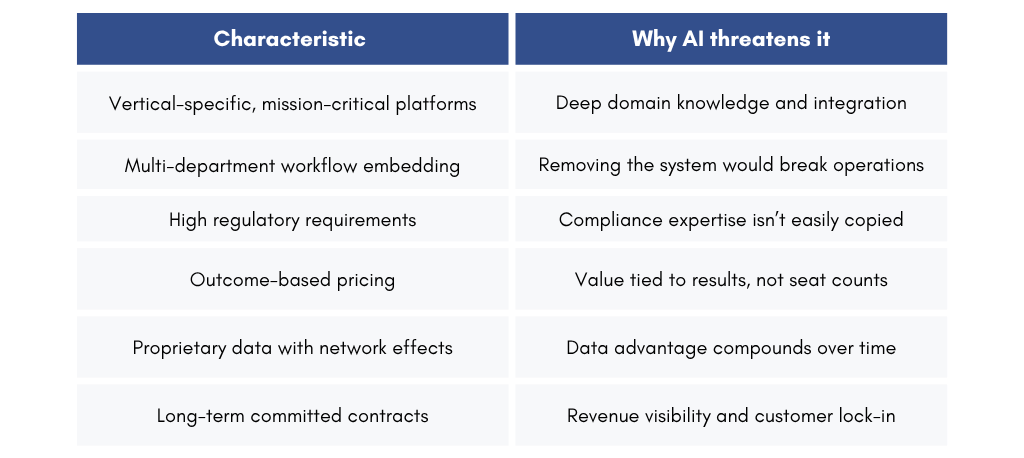

Where we see lower disruption risk:

Across our SaaS holdings, we have not seen genuine AI-driven competitive threats emerge. What we’re seeing is the opposite: companies using AI to reinforce their strengths and move faster on product development. We’re seeing this pattern repeat. Businesses with proprietary data, embedded workflows, and real domain expertise are using AI to extend their lead, not defend against erosion.

Even Anthropic, at “Enterprise Agents” briefing on 24 Feb 2026, highlighted collaboration with leading SaaS companies to further accelerate AI monetisation features.

We are however mindful that the advent of AI and increased cost of inferencing (querying the underlying data) may lead to SAAS companies having to re-engineer their revenue models. Possible changes could include a move from seat based or per using pricing to a model that captures the value of the work being done and the cost of compute to carry it out. An example of which might be a more transaction-based pricing outcome than a purely per user based model

We have been selectively adding to SaaS companies within the portfolio as valuation has increasingly become more attractive. For the first time in a long time, some of these companies are growing faster and cheaper than ASX ex Resources, with better cashflow and balance sheet characteristics.

Disclaimer:

This material is prepared by Paradice Investment Management Pty Ltd (ABN 64 090 148 619 AFSL No 224158) (Paradice, we or us) to provide you with general information only.

This material is not intended to constitute advertising or advice (including investment advice or security, market or sector recommendations) of any kind. In addition, this material represents only the views of the Paradice Australian Equities team as at the time of release and is not intended, and may not, represent the views of Paradice or any of the other investment teams at Paradice.

It may contain certain forward looking statements, opinions and projections that are based on the assumptions and judgments of Paradice with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Paradice. Because of the significant uncertainties inherent in these assumptions, opinions and judgments, you should not place undue reliance on these forward looking statements. For the avoidance of doubt, any such forward looking statements, opinions, assumptions and/or judgments made by Paradice may not prove to be accurate or correct.

The content of this publication is current as at the date of its publication and is subject to change at any time. It does not reflect any events or changes in circumstances occurring after the date of publication.

The information and opinions contained herein, including information obtained from third party sources which are considered to be reliable, are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents.

Subscribe to our newsletter for updates.

Visit our site for individuals and financial advisors.

Visit our site for institutional investors.